Nestled in the “One Big Beautiful Bill Act” (OBBBA) of President Trump is an expensive and ineffective provision which allows employees to reimburse their student loans outside their franchise compensation.

THE tax expenditure was promulgated for the first time in 2020 and expires this year. Under the current law, up to $ 5,250 per year of the compensation of an employee can be used to reimburse his student loans, and these payments are not subject to a federal income or taxes on payroll. The extent of the relief of student loans would cost $ 11 billion Over the next ten years.

When the arrangement was debated for the first time, I argued that instead of relieving borrowers in difficulty, it would rather be a windfall for high -income workers who could have reimbursed their loans without tax alternatives. There are two reasons for this:

- In order to benefit from tax relief, a borrower must not only be employed, but must work for a sufficiently large and sophisticated employer to establish and sponsor a reimbursement plan.

- As with many exclusions and “upside down” deductions, the borrower’s tax savings depend on their tax tranche, the highest-benefit obtaining the greatest break.

Data from the national survey on the remuneration of the Bureau of Labor Statistics confirm these forecasts: the advantages are indeed concentrated among high income workers, in professions requiring four -year diplomas and among large employers.

Student loan services are more common among the most paid workers

High income workers are much more likely to receive assistance in reimbursement of employers’ student loans. Last year, 9% of workers in the upper quartile of profits have access to student reimbursement services, compared to 3% of workers in the lower quartile of the profits (Figure 1).

In other words, around 40% of the program’s beneficiaries appear in the most important 25% of the remuneration distribution – among Americans who have a job – and around 20% are in the most tops of distribution.

In simple terms, the advantages of reimbursement of student tax loans are concentrated in high income workers. Contrading the declared intention of the program to help borrowers of student loans in difficulty, few workers at the bottom of the distribution of income have access to this advantage.

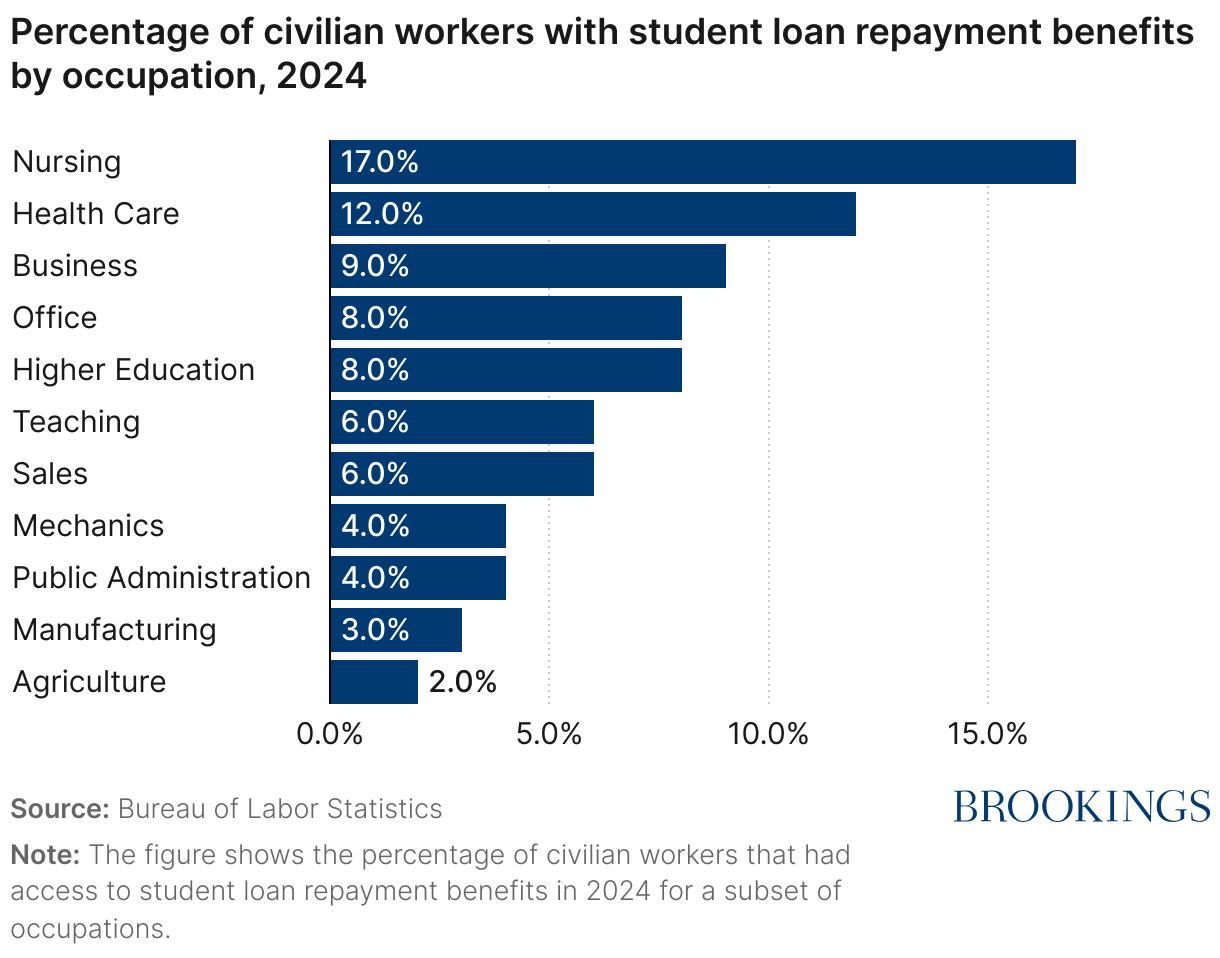

Student loan services are more common among well -educated and white professionals

Nursing is the occupation with the greatest access to reimbursement services for student loans (Figure 2). This reflects the growing number of health care employers using student reimbursement services as a tool to recruit and retain employees. Almost one in five nurse had access to student loan services based on the employer. Other health care professions are second, 11% of workers receiving reimbursement for student loans.

Figure 2

The professions of workers who require less training are much less likely to have access to reimbursement services for student loans. Less than one in 20 workers in manufacturing or mechanics has access to these advantages, while around one in 50 agricultural workers has access to these advantages.

Unsurprisingly, the professions with higher percentages of workers formulated by the colleges are more likely to have reimbursement services for student loans, as employers offer advantages that use their workers.

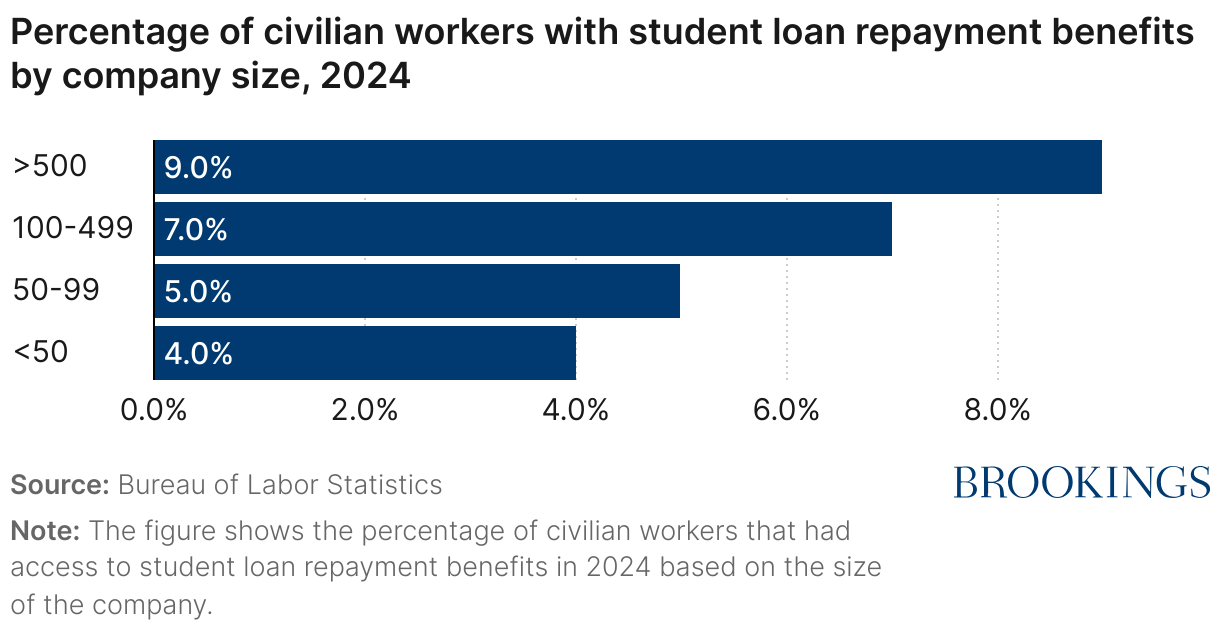

Student loan services are most often offered by major employers

In order to provide tax advantages to employees, employers must establish an education assistance program, which requires a certain level of sophistication and investment on the part of the employer. The implementation of an education assistance program requires that the employer establish a formal written plan, non-discrimination tests, the holding of eligible expenditure files, opinion requirements for employees and tax reports.

Consequently, the largest employers are more likely to provide the advantage (Figure 3). In companies with less than 50 people, only 4% of workers have reimbursement for student loans. This percentage increases to 9% for business workers with more than 500 people.

Figure 3

Conclusion: Access to this tax relief varies considerably according to workers that they work.

Congress has other options

Given the cost of this tax relief for student loans, which is disproportionately benefits high -income -in -white income passes, the congress could consider other ways to use taxes to help borrowers from student loans. An option consists of income -based reimbursement plans, which are available for all borrowers, regardless of their employment status or if their employer offers a reimbursement assistance program. Although these plans have also suffered from administrative challenges resulting from the restrictive requirements of applications and rectification, these questions are dealt with with modest reforms. Despite these problems, the use of these plans is much more widespread than the tax relief of housing for students, and income -oriented plans offer a much better approach to reduce the risk of defect and manage financial charges on borrowers.

The Brooking Institution is engaged in quality, independence and impact.

We are supported by a diverse range of donors. In accordance with our values and policies, each BrooKings publication represents the only views of its authors.